Almost every week, it seems, another part of our world is analyzed in an as-a-service package. This growing trend should not surprise anyone. As hardware, software, bandwidth, and protocols evolve, more processes and resources can be outsourced. This subsequent development is driving digitalization that is transforming industries around the world.

Financial services are no exception. Banking as a Service (BaaS) brings banking to the world. However, as with almost everything related to finance, BaaS is surrounded by mystery.

In this article, we want to overview banking as a service to shed light on its benefits, uses, and challenges.

What is Banking as a Service?

BaaS is a model that allows online banks and third parties to connect directly to banking systems through APIs, building banking offerings on top of a regulated vendor infrastructure, and unlocking new experiences.

Digital-savvy traditional firms can fend off the looming fintech threat by moving into the BaaS space to share their data and infrastructure. In a few years, access to this level of information will guarantee digitally accustomed clients, so banks that start now will be ahead of their rivals and likely to be rewarded with solid demand.

How does Bank as a Service Work?

The BaaS model starts with a fintech, digital bank, or third-party provider (TPP) paying a fee to access the BaaS platform. A financial institution exposes its APIs to TPP, providing access to the systems and information needed to create new banking products or offer white-label banking services.

Besides advancing open banking, traditional institutions that launch their own BaaS platforms are also opening up new revenue streams. The two main BaaS monetization strategies include charging customers a monthly fee to access the BaaS platform or charging for each used service.

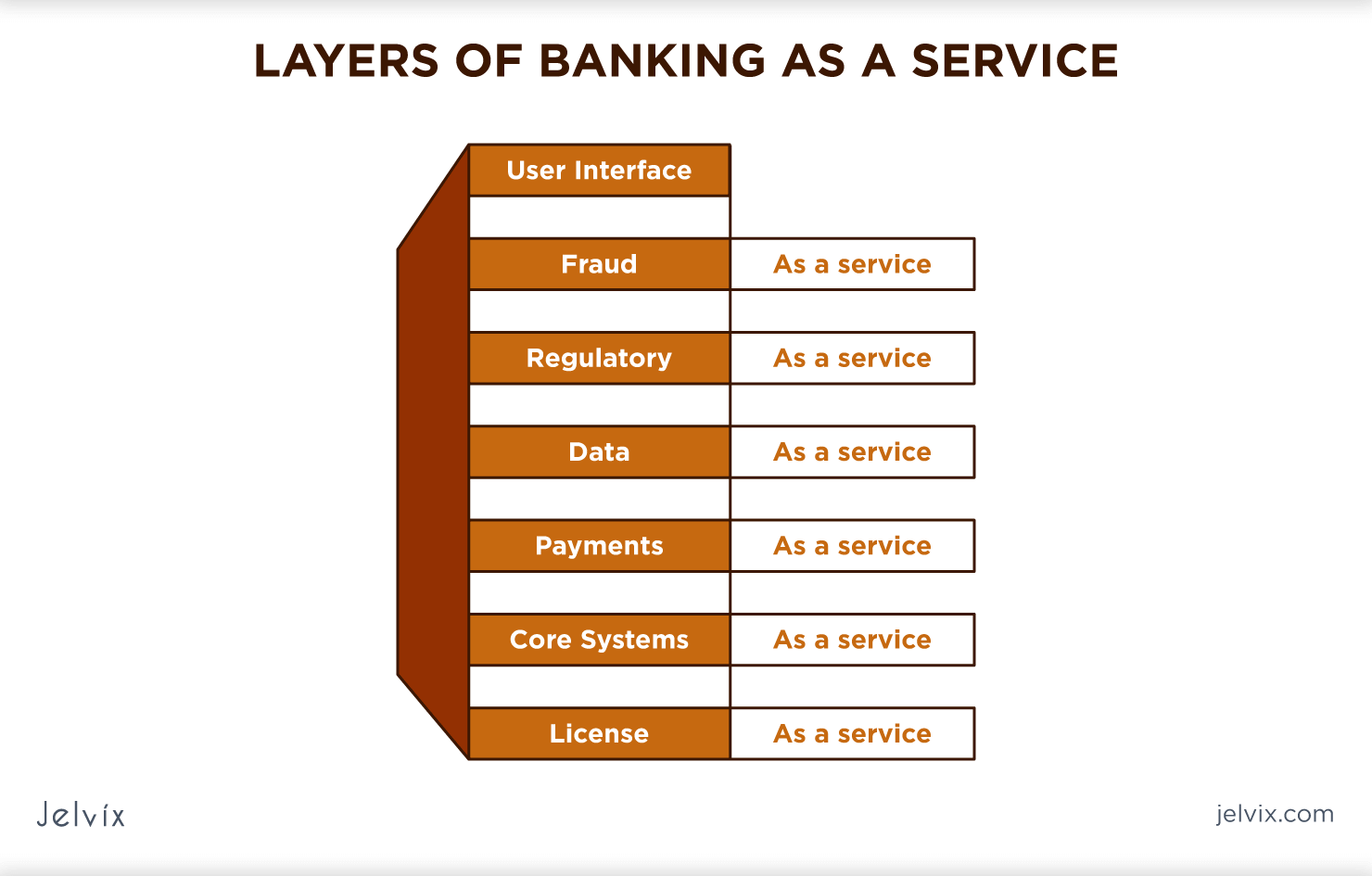

Layers of Banking as a Service

As the image below demonstrates, BaaS can have multiple service tiers, and customers can choose numerous of them for the business. It depends on the needs of the company.

BaaS vs. Open Banking vs. Banking as a Service Platform

You need to distinguish between these three terms. BaaS is often confused with Open Banking as the latter also uses an API to link banks to non-banks. Although, the core functions of open banking differ significantly. Under this model, non-banks use APIs to access banking data and embed it into their financial services. For example, people use a financial management app to keep track of their monthly expenses. The app uses an API to integrate transaction data from the user’s bank account and perform analytics to help them manage finances more efficiently and improve spending habits. The app itself does not provide any new banking services. It simply integrates the data already stored in the bank into the account management functions. This is how open banking business models work.

Unlike open banking, BaaS provides the user with an entirely new type of service. BaaS does not give customers what has already been created but uses it as a basis for making a new banking experience.

Besides, there is a difference between BaaS and a banking platform. The leading players in banking platforms are not third parties but the banks themselves. They use the power of financial technology to provide access to the services offered by the bank. For example, a bank could create an AI-powered tool to help users select the best investment opportunity and quickly complete their day-to-day banking transactions. Currently, financial institutions are using banking platforms to retain clients and enable them to immerse themselves in the fintech industry fully.

In the BaaS concept, the end-user interacts not with the bank but with a third party that offers new services. The brand front-end is connected to the BaaS provider via an API, which connects the provider to the bank. This chain allows distributors, brands, and fintech companies to integrate service banking directly into their products – e-commerce websites, fintech applications, or financial services.

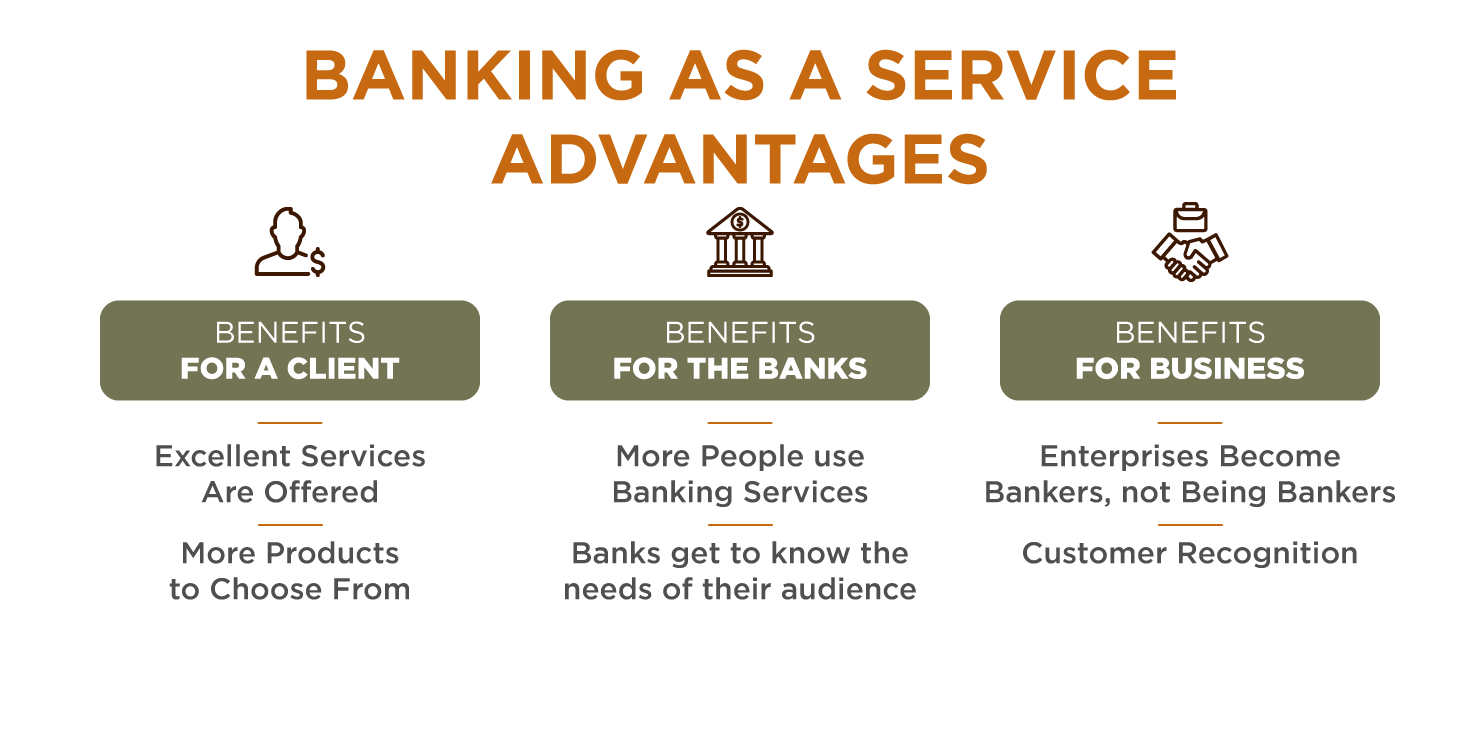

Banking as a Service Advantages

Benefits for a Client

BaaS brings innovation and customization to fund product development. Clients receive the following benefits:

- Excellent Services are Offered

If there were no BaaS providers, customers would use banking services directly. So, it’s not that the client needs BaaS – BaaS requires a client. That’s why BaaS providers strive to offer a truly superior experience. They are making an effort to meet the needs of banking customers who are digital natives and genuinely tech-savvy.

- More Products to Choose From

The wider the choice, the better for the client. High competition is not good news for service providers. But for clients, it gives more flexibility. Innovative solutions strive to be customer-centric and offer all the necessary functions in one place. This enhances financial transparency and simplifies cash management compared to traditional bank accounts.

Benefits for the Banks

Like customers, banks offering API-based data access also have a win-win strategy. At a minimum, they lose nothing and earn more money. Most importantly, they benefit personally from sharing their data with BaaS banking providers.

- More people use Banking Services

Banking as a service does not create an additional burden on the bank. Instead, BaaS provides new lines and revenue streams. The bank offers access to data through the API and takes a commission for this. He does not care how third-party distributors will attract the audience, where they will look for funds, whether they will outperform competitors, etc. They do not need to invest in development. Their primary responsibility is to ensure that customer data is well protected from breaches.

- Banks get to know the needs of their audience

By analyzing the performance of a third-party BaaS provider, banks can gain insight into the needs of their customers. What features do they use, what helps them manage their finances, and what annoys them? Such insights can be obtained using machine learning solutions for finance and incorporated into developing the bank’s products.

Check out successful business tips that help pave the way to the top of the qualitative services and good revenue.

Benefits for Business

Non-banks, enterprises, and fintech companies that provide BaaS play the most responsible role in this game. In addition to the benefits, they may find investing in a new solution challenging, just as it can be when developing any other product. They must build a risk management strategy to avoid failing their idea. But despite the threats, they can still gain a lot of strength.

- Enterprises Become Bankers, not Being Bankers

As FinancesOnline states, payments and settlements are the most popular startup segment among American banking investors. With the fintech industry’s growth, they all see great potential in investing in banking solutions. To offer banking services themselves and circumvent banking laws, businesses prefer to act as a third party and earn money by acting as an intermediary between the financial institution and the customer.

- Customer Recognition

Yes, it is not easy for clients to entrust their financial data to a third-party business they have never heard of. By linking with well-known banking institutions, BaaS providers build on the bank’s reputation in customers’ eyes and quickly gain their trust.

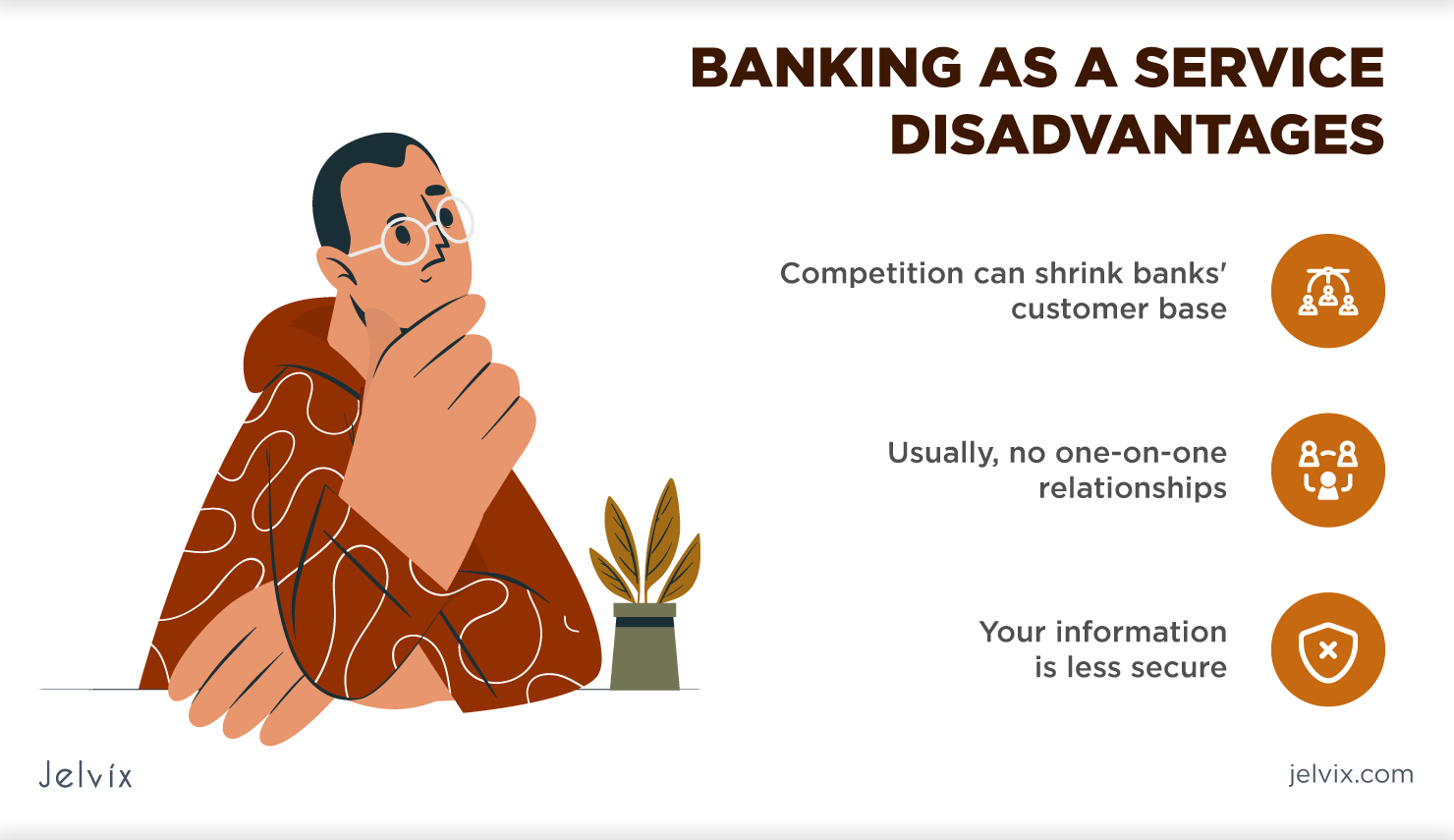

Disadvantages of Banking as a Service

- Competition can shrink banks’ customer base

For banks, BaaS means they face the constant danger of losing some of their market share to better-serving non-banks.

- Usually, no one-on-one relationships

If you prefer digital banking but want to interact with your financial institution in person, you generally won’t get it with BaaS accounts.

- Your information is less secure

Because you use two companies for your banking transactions (the account offering company and the bank), your information is exposed in two ways instead of one.

Banking as a Service Examples

To get a better understanding of BaaS, let’s take a look at a couple of real-world applications. This list is not definitive and is growing every day, so we will analyze three options for using banking as a service:

- Platforms and marketplaces with a large user base can benefit significantly by offering their customers the e-wallet functionality through deposit accounts. For example, crowdfunding platforms can use a BaaS solution to create unique IBAN accounts for individual users and hit two birds with one stone. Firstly, it contributes to a better user experience as they do not need to make a bank transfer every time they make a transaction on the platform as the funds are securely stored there. Secondly, it is easier for the platform to convince customers to reinvest, significantly increasing client retention.

- Almost any service provider can benefit from BaaS and offer white-label payment cards to their clients. Customers take advantage of individual card programs, and businesses create an additional revenue stream.

- However, fintech startups are taking full advantage of BaaS services. They can use the infrastructure and functionality of banks (also known as banking software as a service) and data banks about their customers. This opens up a whole new spectrum of startup opportunities, from personal finance apps to real-time payments, from targeting niche customers to focusing on mainstream adoption. What is paramount for startups is that BaaS can save you a ton of money and at least a couple of years in business and product development. Not to mention that they would not need to have the funds to acquire a license. The earlier they enter the market, the happier their investors are.

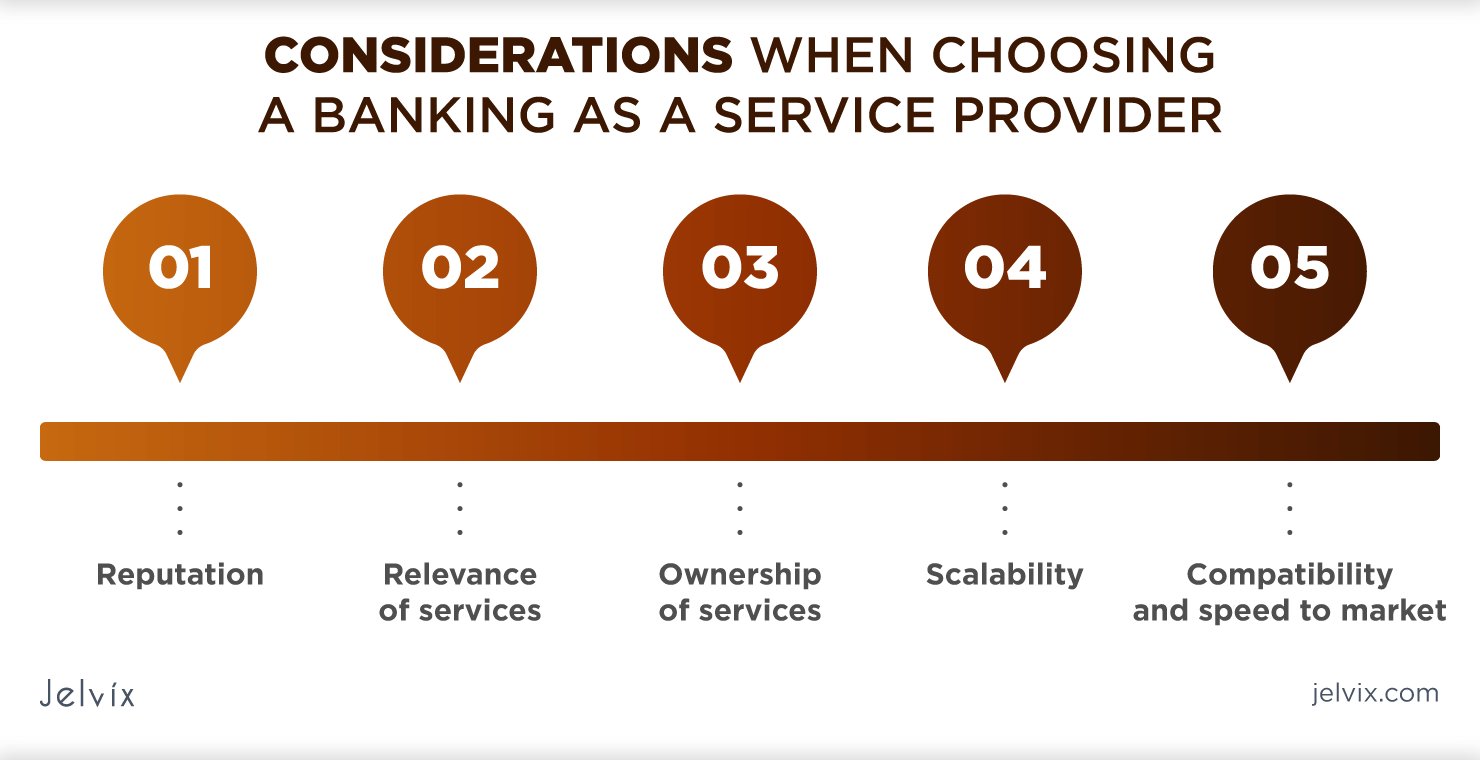

How to Choose a Banking as a Service provider?

So you’ve decided to integrate your business with a financial services platform. When searching for the ideal BaaS provider candidate, we suggest considering the following:

- Reputation

In the global network, nothing stays a secret for long. Look for reviews and testimonials to form an objective opinion.

- Relevance of services

Take a close look at the services offered by a particular provider to ensure they meet your business requirements.

- Ownership of services

Are the proposed APIs and solutions provided by the company or owned by third parties? This issue will become necessary as the partnership develops.

- Scalability

Does the potential partner have the tech stack, resources, and stamina to play the long game? Will they be able to stay up-to-date as their customer base expands and business needs grow?

- Compatibility and speed to market

How quickly and reliably can the supplier deliver the solution you need? There is one more small difference that we should mention to avoid any confusion.

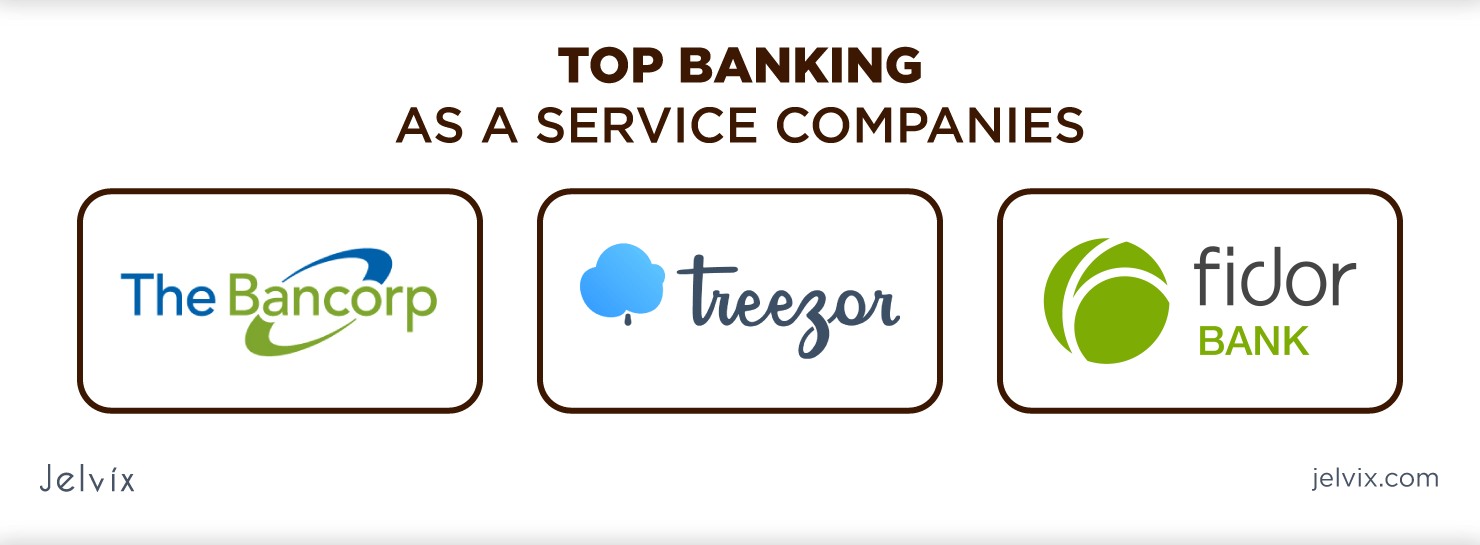

Top Banking as a Service Companies

As BaaS gains momentum, new providers are entering the market along with platforms created by banks. While BaaS providers use a closed architecture, platforms are designed to share APIs with clients. Here are some of the leading players.

- The Bancorp

With $6.2 billion in assets and $232 billion in annual cumulative processing volume, The Bancorp started as a branchless bank and is now a leader in digital financial services. The company provides private banking and technology solutions for non-banking businesses. It has been holding the number one position in prepaid card volume in the US for eight consecutive years and specializes in institutional banking and commercial lending.

- Fidor Bank

This German company, founded in 2009, has gone as far as creating its own BaaS platform. It runs on a proprietary OS and is a cloud-based modular system. Fidor’s teams have created over 40 standardized, forward-thinking APIs that integrate seamlessly with any customer service. The Fidor mobile banking app covers everything from standard accounts and card transactions to loans and crypto investments.

- Treezor

Treezor is a Paris-based banking platform as a service, a “one-stop payment solution.” Recently acquired by Societe Generale Group, thanks to their innovative expertise, the startup is accredited to provide personalized payment services to its customers.

Challenges of Banking as a Service

The challenges of implementing a BaaS strategy are numerous. Fortunately, related solutions pave the way for user-friendly financial products and solutions. Let’s dig deeper.

- Modernization of traditional banks

The core systems of most traditional banks are outdated. They are incompatible with modern technology. This can be a significant problem when implementing a BaaS model, as it can interfere with third-party integration.

The future of banking as a service will include a modernized architecture of traditional banks. This will help expose services, products, and processes such as APIs.

- Changing roles of players in the financial industry

Recent research shows that traditional banks are slowly losing the “customer trust” advantage over fintech players. On the other hand, many tech companies like Apple Card enter the financial space because they have customer trust.

Moreover, BaaS involves cooperation with third-party players. Naturally, there are many coincidences in terms of functionality. In addition, many companies use ‘white labeling’ when offering their products. This can confuse end customers.

Given these points, the future of BaaS shows a massive shift in player responsibilities.

- A well-defined API strategy

Opening a bank or business (middleware) via an API is no small feat. Operational processes and business opportunities must be presented optimally. However, most organizations face challenges when creating an API strategy.

The main goal when creating an API strategy should be ease of integration. It should provide maximum business value by limiting the cumbersome aspects of integration. The future of the financial industry may include a global standardization of the API strategy.

Considering all factors, the BaaS sector shows no signs of stopping. It would be interesting to see how technological progress will affect the BaaS model in the next decade.

The Banking as a Service Future

The financial sector is rapidly changing, and BaaS is paving the way for a new reality. Banks, fintech, service providers, and brands can achieve synergy by creating functional and efficient integrated solutions. In an interconnected environment, everyone will reap their respective benefits if they quickly adjust their strategy.

As financial services more closely reflect consumer needs, BaaS providers will attract new customers. Better customer profiling and additional revenue streams will give merchants a well-deserved bonus. All vendors need to do is establish relationships with a few relevant merchants and manage them effectively. The benefits for the banking sector from merging with providers and brands and reaching a much wider audience are even more apparent.

Conclusion

As you can see, BaaS has its benefits and challenges, just like any other development case. But it is a relatively vacant niche that gives you higher chances to stand out from the rivals. If the banking industry in your country is well-developed, you can create a BaaS solution and expand your market share.

If you are into building a fintech product, contact the Jelvix team. Our experts will be glad to help you with everything from strategy planning to software development and testing.

Need a certain developer?

Access top talent pool to reach new business objectives.